(Posted July 2025)

Net present value (NPV) is a common quantitative analysis required on the CPA Canada Common Final Examination (CFE). This blog summarizes the key technical you need to apply, as well as some common mistakes candidates make when preparing an NPV analysis.

When to Use

NPV is used when trying to decide whether to proceed with a limited life investment or to choose between alternatives. It discounts the incremental cash flows associated with the investment. If the NPV is positive, then the company should proceed with the investment from a quantitative perspective. NPV is considered the best quantitative tool for capital budgeting decisions. It is a direct measure of the expected increase in the value of the company.

Components

Upfront cash flows – These are cash flows incurred before the start of the project and these costs are not discounted. Depending on the nature of the upfront cash flows, you will need to consider whether you need to apply a tax shield to these costs.

Ongoing cash flows – These are cash flows incurred during the project. It is important to use cash flows and not income. All incremental cash inflows and outflows of the project should be considered except financing impacts (see below), including the tax impact of the cash flows.

Time period – You are typically given the expected useful life of the equipment or the time frame of the investment, which will tell you how many years to include in your NPV analysis.

Discount rate – In some cases, you will be provided with a discount rate and in other cases, you might be told the company’s cost of capital, or you might have to calculate it.

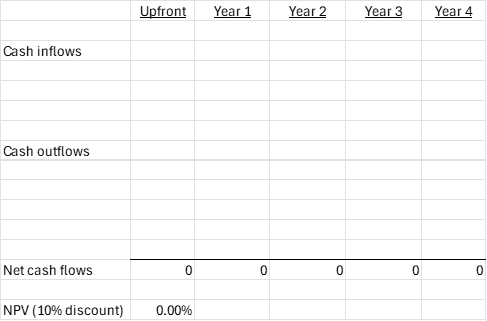

Format

In our CFE Prep courses, we talk about how to be efficient with your quantitative analysis. One of the ways you can do that is to set up your calculation before you get started. This is easy to do with an NPV analysis because it typically includes the same components (cash inflows, cash outflows, NPV calculation). When you set up your calculation, including formulas, in advance, it means that you can then use almost all of your remaining writing time to insert adjustments. When you need to stop because you need to conclude on your analysis, you will already have an answer waiting and you do not need to worry about not yet having calculated the actual NPV.

Here is a sample set-up for an NPV analysis. Notice that the formulas to sum the cash flows and calculate the NPV have already been inputted, so now you can simply slot in the cash flows.

Common Mistakes

Financing impacts

Interest expense is not included in an NPV analysis because the interest cost is inherent in the calculation due to the present value factor. If it is included in the provided earnings or cash flows, you would add it back to avoid double-counting.

A similar issue occurs with including debt repayments. Debt repayments include both interest and principal. You already know why interest is omitted, but you also need to omit principal repayments because whether the project is profitable or not should not depend on whether the company is leveraged or not. What if a different company invests in the project and does not require financing? If debt repayments are included, there would be two different NPV amounts for the same project due to those financing differences.

Discounting

We often see candidates make errors in using the correct formulas to discount their analysis. If you choose to use the NPV formula in Excel, it is important to note that Year 0 should not be included and should simply be added to the result afterwards. If year 0 is included, that would result in discounting year 0, which is not appropriate.

You can also use the PV formula in Excel to present value each year as appropriate (each year’s cash flow is the FV for that year) and then sum the present values. When candidates use this approach, they are sometimes confused over how to deal with multiple years where the cash flow does not change. While you can still efficiently do this with the copy and paste function in Excel, it is much more efficient to determine the present value of the annuity over those years and then discount it back to year 0. For example, if I had a cash flow of $100,000 in years 3-5, I could take the NPV of the annuity over 3 years [=PV(10%,3,-100000)] and then discount this back two years to year 0 [=PV(10%,2,,-248685.2)].

Upfront versus ongoing costs

We often see candidates get confused over where to put the upfront costs in their calculations. Upfront costs should be placed in year 0 (or an upfront or initial column), and those costs are not discounted. We often see candidates adding them to year 1, which impacts the accuracy of the NPV calculation and typically means you will not get credit for that item.

Other cash flows

Sometimes, there are other cash flows provided in the case facts that can seem tricky. The important thing is to pay attention to the nature and the timing of those cash flows.

For example, you might have information on the salvage value of the investment at the end of the project. In this case, you would want to have a cash inflow in the final year of your analysis, discounted back to account for the cash the company expects to receive at the end of the investment.

Another example could be that a piece of equipment is purchased midway through the investment time horizon. In this case, it would be discounted based on the year it is acquired, and you would want to consider the tax shield impact of the equipment at that time.

Conclusion

Remember that you need to conclude on your analysis. This is more than just stating what the NPV of the project is. You need to answer the user’s question and consider the impact of your analysis. Should they proceed with the investment? Depending on the required, you may also need to consider qualitative factors before making an overall conclusion.

More detailed information on how to approach an NPV analysis is included in our Scenario Flowcharts Workbook and Skill Drills, which are included in our CFE Prep courses, and in our Competency Map Study Notes publication.